For the last three years, the NZ Herald has asked approximately seven investment firms for their shares predictions for the year ahead. Each firm picks five companies they think will perform the best and the Herald publishes their picks. Here is a link to the 2019 picks.

So, how did they do?

ACTIVE STOCK MANAGEMENT RESULTS

2019 stock picking rankings

These firms don’t tend to publicise all their costs, so I have assumed a total cost of investing of 2.5%. This includes brokerage, administration and management costs. With the market index fund I have assumed 0.5% investment fees.

Not a bad result for the active managers is it? Even after consideration of their higher costs, four out of seven firms outperfrom the index, and three of them by quite some margin. Then why would I recommend index funds as a great way to invest?

To answer that question let’s have a look at the 2017 and 2018 results from the same investment firms:

2017 stock picking rankings

2018 stock picking rankings

The top ranked company from 2018 (Vulcan Capital) was the lowest ranked company for 2019. Note, they have changed their name to Foster Stockbroking. Goes to show how a change in staff can severely impact performance. How can you know this ahead of time? You can’t. With passive investing you don’t need to worry about things like that.

Out of 7 companies in 2017, only one now has consistently beaten the market index. Craigs Investment Partners. 5 companies in 2017, 2 in 2018, and 1 in 2019. This inconsistency makes it nearly impossible to pick the winning investment firms, especially over the long term.

We will now look at the average returns over the last three years.

AVERAGE IS NOT AVERAGE

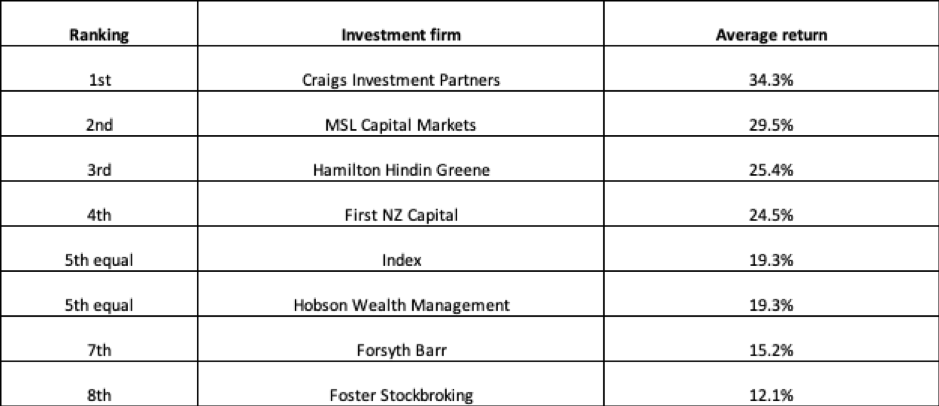

Average three year returns of stock pickers

We already knew Craigs Investment Partners had outperformed the index over three years due to being the only active manager to outperform the index in each of the last three years., But we can also see that there are four other companies that have outperformed the market index thanks to a great ‘good’ year/s compensating for their ‘bad’ year/s.

But are these averages correct?

No they aren’t. When it comes to investing it is the compounded average returns that matter.

Compounded average three year returns of stock pickers

To be fair, there is not too much movement except for First NZ Capital swapping places with Hamilton Hindin Greene. Even though First NZ Capital have a lower average, their ending balance is higher. But how does Hamilton Hindin Greene have a higher average after fees return than First NZ Capital (25.4% vs 24.5%), yet deliver less money in the hand?

The answer is in the compounded average, which is different to the simple average.

How do we explain this phenomenon? Say our $10,000 grows 100% in the first year to $20,000. The following year our investment falls 50%, taking us back to our original amount of $10,000. Over 2 years then, our annualised gain is zero. However, an adviser who is keen to put a positive spin on the numbers may tell us that our return is actually 25% (50%/2). This is the average return and as you can see in the tables above, is very misleading.

In real life, we only realise the compounded return, not the average annual return many brokers and fund managers claim. So, please don’t be fooled by the numbers. When someone gives you the average return from the stock market, it may not be the real return.

Negative returns are what make the biggest impact. Say we have $50,000 to invest and experience 20% returns in our first year. At the end of the year we will have $60,000. In the second year we lose 20%, so back to $50,000 right? Wrong. Even though the average return is 0%, we have actually lost money. A 20% loss on $60,000 is $12,000, taking our year 2 balance to $48,000. $2,000 less than we started with. A compounded return of minus 2%.

Whenever we lose money, it takes a greater return just to break even. If we lose 20%, we must earn 25% to get back to where we began. The more we lose, the worse it gets. Lose 50% and we need 100% to get back to even.

On the flipside, gain 100% and we only need to lose 50% to get back to even. This is why it is so important when investing to lower our downside risk and protect our gains as best we can to minimise our exposure to losing money. It’s much better to have compounding working for us and our gains, than against us with losses.

The large 19.3% loss incurred by Hamilton Hindin Greene’s picks in 2018 is the reason why their annualised compounded average is much lower than the simple average. This is why they drop a place on the table.

And this is the nature of active investing. It is much higher risk than passive investing. Yes, you may have some great years, but you can also have some terrible years too. Check out this table that shows the variations between the best returns and the worst returns, otherwise known as volatility.

Range of investment returns of active funds

Unsurprisingly, the index has much lower volatility than most of the actively managed funds. Although Craigs Investment Partners have the lowest volatility and the best returns, this can easily change with one bad year. It is the ideal though, best returns and lowest volatility.

TAKE AWAYS

The stock picking exercise the Herald does is just a game. It is not real money and picking just five companies is fraught with danger. Investing in such a low number of companies is extremely risky and is not diversified enough.

Regardless, these are the five companies that these companies think will perform the best. With the exception of Craigs, how can companies get it so right one year and so wrong another year? It seems that a lot of a companies returns are based on pure luck. Why then pay someone 2.5% in fees for a possible chance to beat the market, but by no means guaranteed? We can see by the results that there is a lot of inconsistency and trading places between the companies.

And with so much inconsistency how can you know ahead of time which investment company it is that will perform the best in any given year?

After three years, there are still four investment companies outperforming the index and three underperforming. I can guarantee that in 20 years time there will be less than four of these companies still outperforming the index. This number will drop. This is because it is hard to consistently outperform over longer periods. With each passing year, fewer and fewer investment companies can keep up with the index.

Do you know which company (if any) will outperform the index over this time? I don’t. There may be one or two, but which one?

If you pick the wrong one, then you will end up paying high fees for sub par performance.

FINAL THOUGHTS

I am not here to advise against investing in actively managed funds. Some of my portfolio is in active management, albeit a very small portion. I understand the risks but am willing to take on that risk for a small chance at outperformance. But I definitely wouldn’t go active for my whole portfolio. I am just advising on some warnings.

Warnings on how difficult it is to consistently outperform the market index and to know ahead of time which investment companies will be better than others.

Warnings as to how high fees can make poor active performers even worse performers.

Warnings as to how active fund managers report their returns. Average returns are not accurate and the number you should be calculating is the compounded returns. The difference can be quite substantial, especially if one investment company has wild variations in returns.

Warnings that actively managed funds often invest in less companies than the market index. This can potentially lessen diversification and increase risk. In turn, this increases volatility, resulting in higher gains and higher losses. As we saw earlier, minimising losses is critical due to losses needing higher gains in order to recover.

Warnings that actively managed funds often do not report their losers. For example, if company A started the year at $2 per share and was made bankrupt during the year taking their share price to zero, the investment company that invested in that company may decide to exclude that companies negative 100% returns from its end of year returns. They can just remove the company from their end of year holdings, making their returns look much better than they really were.

I must say though, personally it is nice not having to worry about the performance of individual companies. With index funds, I can just invest in the whole market and not worry about who is performing and who isn’t. That peace of mind of a low cost, hugely diversified portfolio is very freeing and allows me to just get on with more important things.

For more information on investing, you can read the beginners guide to investing here.

This will be the last year I write this blog post as I think you all get the idea. NZ herald has now made this competition amongst the brokers paid content, so I can’t view it as a non subscriber.

The information contained on this site is the opinion of the individual author(s) based on their personal opinions, observation, research, and years of experience. The information offered by this website is general education only and is not meant to be taken as individualised financial advice, legal advice, tax advice, or any other kind of advice. You can read more of my disclaimer here